Products

Products

Solutions

Solutions

Resources

Resources

-min%20(1).avif)

“I recommend SurePayroll to everybody. I tell them, ‘Just go through SurePayroll and you’ll never have to worry about anything.’”

-min.avif)

“Being able to depend on SurePayroll to run payroll and handle payroll taxes gives me tremendous peace of mind.”

-min.webp)

“SurePayroll is easy, affordable, and it saves me time and headaches. I don’t have to figure out how to do payroll and taxes because SurePayroll does it for me.”

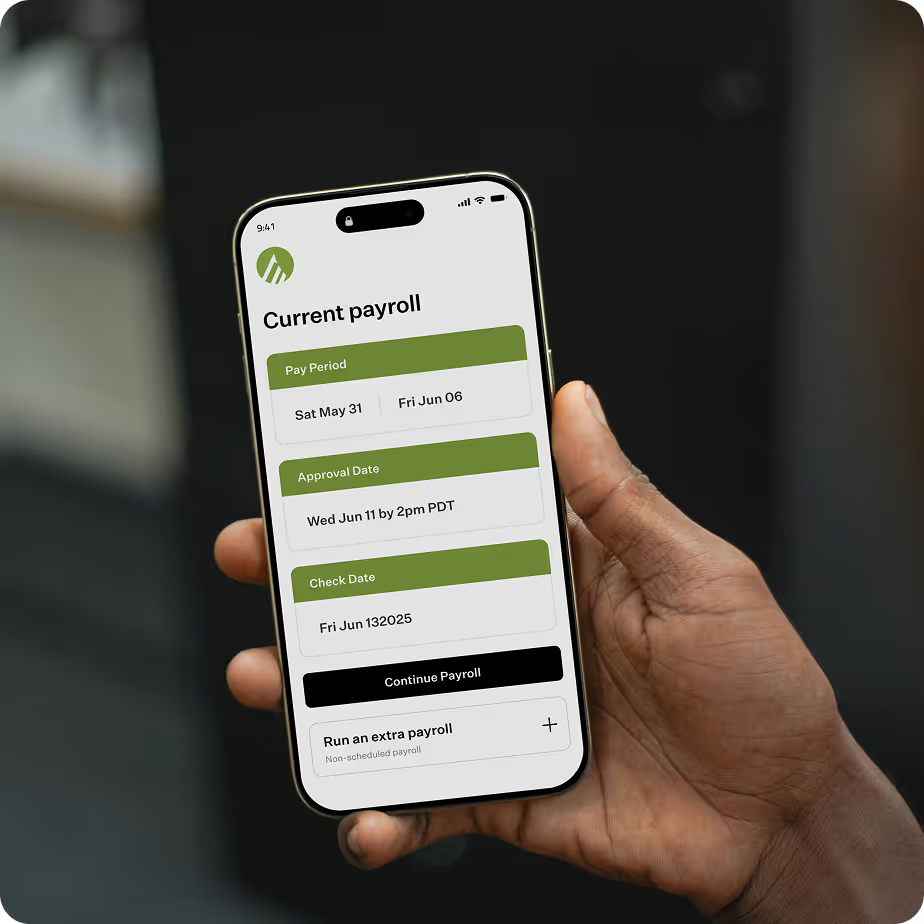

You can run your clients' payroll. Or they can run it themselves. Either way, it’s just a few taps. Click. Run. Done.

Once you set up your custom portal, your customers see your brand, not ours.

Our simple cost structure makes it easy to resell payroll at a profit. Plus, you can add, pause, or terminate service for any client at any time.

We’ll calculate and file payroll taxes on your clients’ behalf. (Agency notice pops up? We can help figure it out.)

When your clients go to their portal, they’ll see your brand. (You can even embed payroll directly on your site.)

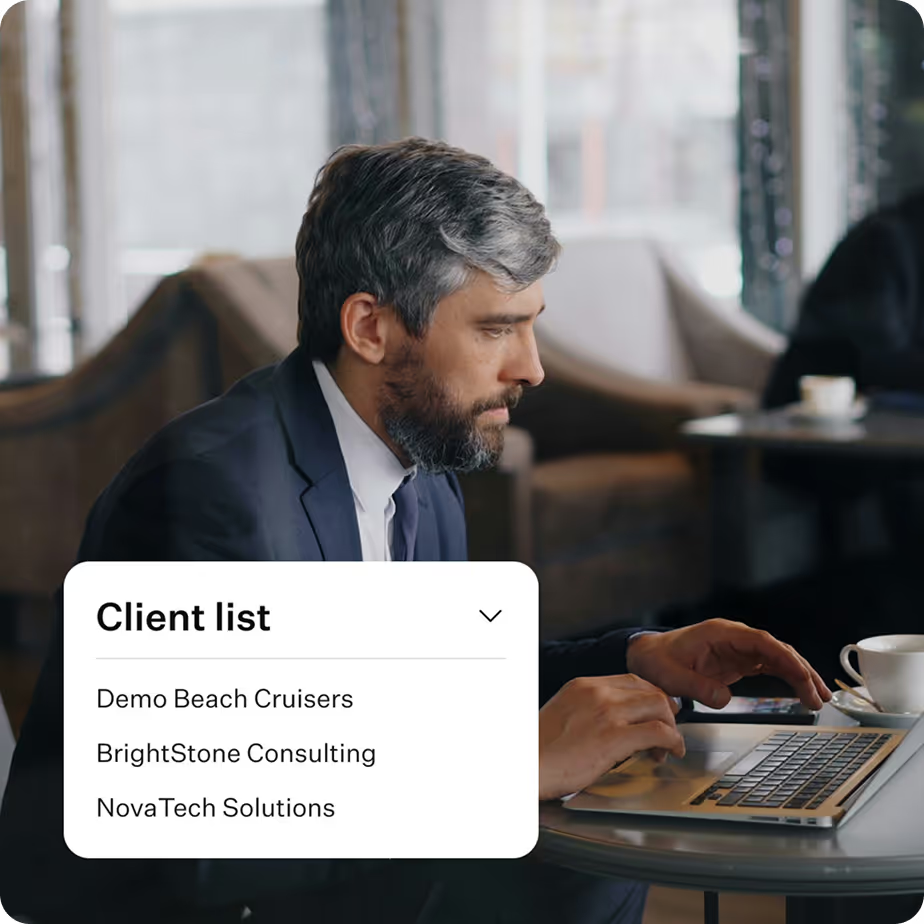

Clients can run payroll themselves—or you can do it for them. It’s all in one simple, clean portal.

Need access to our dedicated Accountant Care Team during business hours? Just pick up the phone.

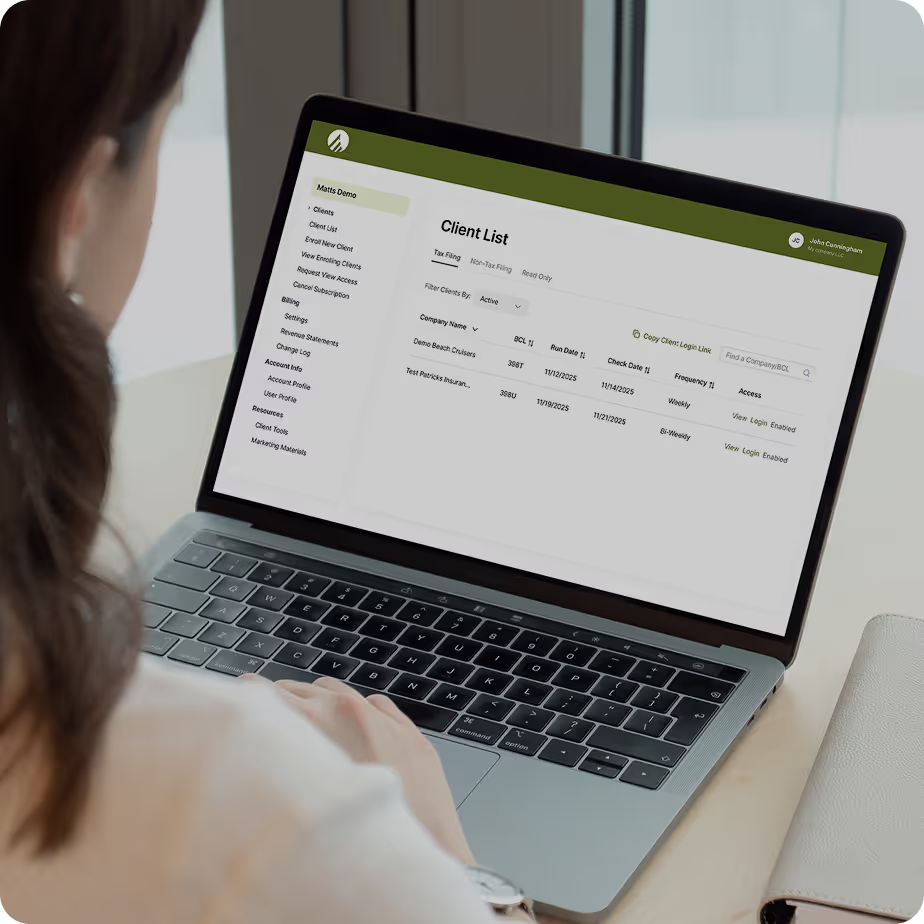

Everything you need to provide great service is in one central dashboard.

Run payroll for your clients in a few taps (or set it up to run automatically).

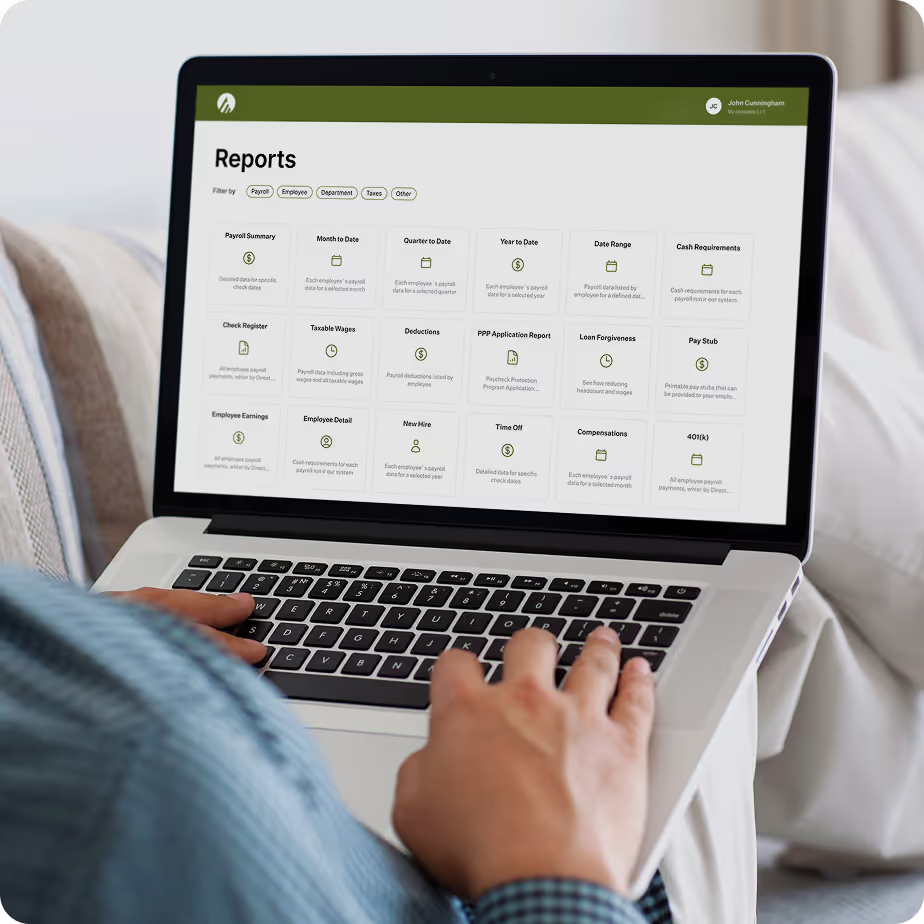

Easy sorting. Easy reporting. And you can sync your client’s payroll info directly to your general ledger.

Our pricing is predictable, straightforward, and designed to help your firm turn a profit.

Offering a payroll service with SurePayroll is a simple, low-effort way to make more money.

Payroll service adds another vital client communication touchpoint—helping you strengthen relationships. (Plus, the more services you provide, the harder you are to leave.)

When you offer payroll, you’re no longer “just a tax service.” You’re full service. You’re a vital part of how your clients run their businesses on a week-to-week basis.

Lots of small businesses spend hours every month running payroll from a spreadsheet. Show them an easier way and they’ll love you for it.

.avif)